In line with expectations, the South African Reserve Bank (SARB) MPC maintained the policy rate at 3.50%. It was a unanimous decision, in line with our thinking, breaking the 3:2 split in the 5 person committee in the prior 3 meetings.

The balance and tone of its March statement was always going to be more important than its decision itself to hold, in our view. Indeed this proved true where the MPC managed to strike a balanced tone in its statement and Q&A, perhaps with a small hint of dovishness implied by its modestly softer core CPI projections (-0.1pp to 3.3% average for 2021 and unchanged at 4.0% for 2022); expectation for a negative quarterly GDP growth performance in Q1 (in line with our call) and warning over the delay in the country’s vaccine roll-out and inevitability of a “third wave” of infections over the coming months.

Unsurprisingly, it made some upward revisions to its headline CPI projections for 2021 (+0.3pp to 4.3% average), though we point out that this was almost entirely down to higher oil prices which it now sees averaging USD 62/bbl from USD 50/bbl previously. In the same breath, however, it toned down its 2022 and 2023 CPI projections by a tenth of a percentage point to 4.4% and 4.5% respectively (firmly anchored at its 4.5% inflation target mid-point), helped also by a stronger starting point for the ZAR in its models (14.96/USD versus 15.70 previously).

Describing the inflation outlook as “balanced”, the SARB is clearly less concerned at the impact of exogenous price pressures on the broader inflation picture – a point we have argued extensively in South Africa: GDP deflator reinforces core CPI view, dated 18 March. Importantly, the release of Q1 inflation expectations from the Bureau for Economic Research (BER) in conjunction with today’s statement would have further helped the case for low for longer rates, we believe. These slipped 0.3pp to a record low of 3.9% in 2021 and 4.2% in 2022 respectively. Indeed 5y expectations also continued to grind lower to within a tenth of a point shy of its 4.5% target midpoint.

Fig 1: Inflation expectations still sliding lower

Sources: BER, BNP Paribas

Bottom line: Faced with a potentially difficult communication task this week, we believe that the SARB managed to put together a well-balanced statement that has begun gradually aiming to tone down expectations of aggressive rate hikes currently implied by markets over the next 12 months.

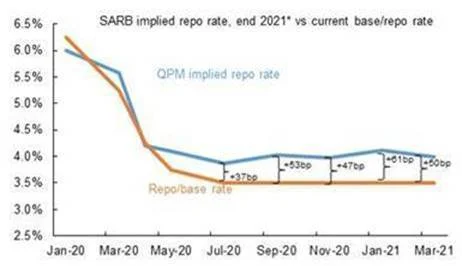

Indeed slightly softer core and modest downward revisions to its outer year headline CPI estimates allowed it to soften its end year repo rate implied by its QPM by 11bp to 4.00% and unchanged at 4.95% by end 2022. The inflation ‘steady-state’ configuration of this model, however, now indicates the first 25bp hike earlier (Q2/May 2021) versus its previous output implying hikes in H2 2021. We would argue that this is largely technical, however, and is owing to the expected spike in headline CPI in Q2 which can be ascribed almost entirely to higher fuel inflation and base effects. With the economy likely to contract in q/q terms in Q1, we would be surprised if the SARB dogmatically stuck to this path – it continues to cover itself in this respect by indicating that its QPM is merely “a guide and can change from meeting to meeting” and that the MPC will “continue to look through temporary price shocks”.

As data evolves (importantly we don’t believe that this week’s lower than expected February CPI print was incorporated in its latest model outputs), we would expect further moderations in its core CPI estimates in the coming meetings, allowing its QPM to push out the timing of policy normalization.

It therefore remains about the data moving forward. Given our sub-consensus views on both GDP growth and inflation (particularly core), we remain comfortable in our view for the SARB to only begin normalizing rates from Jan 2022.

Fig 2: Lack of more hikes implied by QPM gives the statement a more dovish tilt