The growth of the digital economy has already distorted many industries, from media to transportation, just as technology has changed the face of payment systems. Next in line? Money itself.

Currencies have taken on many shapes and sizes over the past seven centuries – from the Yapese who used 12-feet stone wheels called rai when executing exchanges, to the famous ‘gold standard’. However, ask any monetary economist when the tide changed for money as we know it and they will say August 15, 1971. A historic day indeed when then US President Richard Nixon directed his secretary of treasury to temporarily suspend the convertibility of the dollar into gold or other reserve assets – ending the gold standard and migrating the dollar to today’s fiat standard.

Because almost all economies use the dollar as their reserve currency, the unbundling of the US from the gold standard meant money supply (M3) was no longer tethered to national gold reserves and consequently, M3 has grown exponentially over the past 47 years.

The financialisation of economies since the 1970s has contributed to the need for electronic payment systems.

But with money supply at its peak and debt at unprecedented levels, what is the next frontier for fiat money?

Fiat money demise

Along with exponential growth in money supply over the past 40 years, credit has expanded drastically, ushering in the quintessential shopper accessory – the credit card. Today, Visa and Mastercard control more than 80% of the global credit card market.

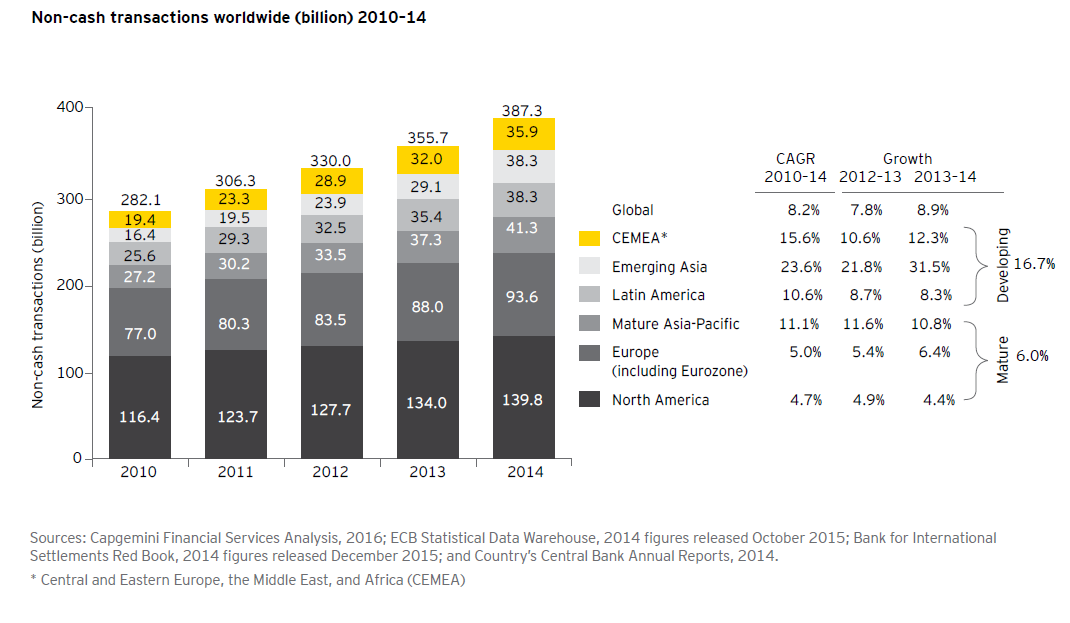

However, developments in fintech in the past decade have seen mobile money disrupt the playing field.

There are now an estimated 12 000 fintech companies, which are fostering the adoption of non-cash transactions.

Millennials have hastily accepted new payment method, with some hardly conducting transactions with paper notes anymore. Buoyed by a surge in the digital economy and smartphone penetration, unorthodox financial services have gained ground. Also, as the internet of things gains ground, payment systems have evolved with an emergence of machine-to-machine transactions.

Moving beyond mobile money

Arguably Kenya’s most famous contribution to the world after the word ‘safari’ is mobile money. The M-Pesa platform – an SMS payment service that boasts over 30 million users in 10 countries today – reached over six billion transactions in 2016. That’s 529 transactions per second.

Mobile money has also become the face of financial inclusion in many developing countries, with banks embracing the platform.

Grant Niven, EY’s advisory financial services director for the Middle East and North Africa, says: “While there is still work to be done to get banks, operators and market participants to integrate efforts to drive financial inclusion, private sector solutions that bridge the gap between mobile money and banking are also growing in number.

“These include eTranzact, operating in five countries, and txtNpay and expressPay in Ghana, which enable consumers to bank and pay bills.”

Away from the private sector, mobile money could birth an African digital currency.

“The next evolution of digital enablement in Africa is likely to progress to government-issued digital currencies with [the] imminent eCFA launch, the name of its digital currency, by the West African Economic and Monetary Union,” says Niven.

“Beyond the centralised concepts of money, the advancement and adoption of peer-to-peer based blockchain technology to increase global interoperability of money across borders is likely to advance rapidly.”

This article was written by Arnold Segawa and sourced from MoneyWeb; for the original article, click here.